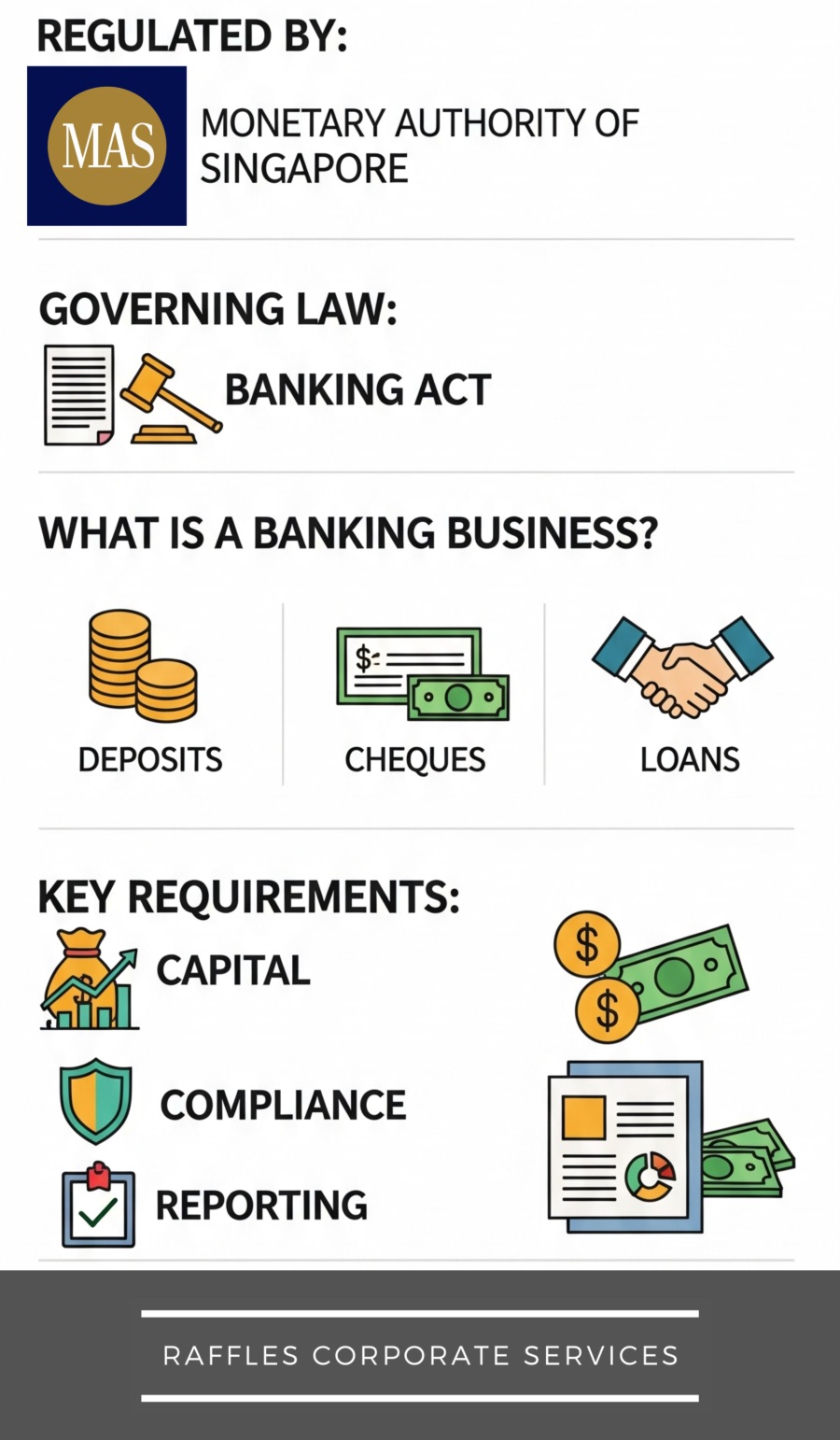

Banking licenses in Singapore are primarily regulated by the Monetary Authority of Singapore (MAS). MAS acts as Singapore’s central bank and is the unified supervisor for various financial institutions, including banks.

Here’s a comprehensive overview of banking licenses under MAS regulation, drawing from the provided sources:

- Regulatory Authority and Legislation

- The Monetary Authority of Singapore (MAS) is the national regulator responsible for supervising the banking industry in Singapore. It has powers of intervention and inspection to ensure market effectiveness and order.

- The main legislation governing banking licenses and the business of banking in Singapore is the Banking Act (Cap 19). This Act is further supplemented by Banking Regulations.

- Banking corporations are also subject to MAS control under sections 3 and 4 of the Financial Services and Markets Act 2022.

- Definition and Scope of “Banking Business”

- The Banking Act specifically regulates “banking business,” the licensing of banks, capital requirements, banking secrecy, and control over banks.

- “Banking business” is defined as:

- Receiving money on current or deposit accounts.

- Paying and collecting cheques drawn by or paid in by customers.

- Making advances to customers [Corporate Governance -Practice and Issues.

- MAS has the authority to prescribe other activities as banking business, though no additional activities have been prescribed to date.

- Deposit-taking activities by banks are primarily governed by the Banking Act.

- Entities Requiring Licenses or Approval

- A “banking corporation” is explicitly defined as a bank or merchant bank licensed under the Banking Act.

- Broadly, MAS licenses or approves various “financial institutions”.

- MAS approval is required for any person intending to acquire a substantial shareholding in Singapore-incorporated banks or financial holding companies, among other financial institutions. This also applies to a person obtaining 5% or more interest in voting shares in companies engaging in certain industries, including Singapore-incorporated banks.

- Key Requirements and Obligations for Licensed Banks

- MAS issues detailed notices and directives to banks and other financial institutions. These cover extensive requirements for:

- Capital adequacy and reserve requirements. For instance, MAS Notice 637, issued under the Banking Act 1970, relates to capital adequacy requirements for banks incorporated in Singapore.

- Board and executive appointments, including requirements for a strong and independent element on the Board.

- Conflict principles.

- Disclosure rules, audit, and reporting requirements.

- Insider trading rules and money-laundering rules. Banks in Singapore must ensure their collection, use, and disclosure of personal data comply with MAS requirements for preventing money laundering and countering the financing of terrorism (AML/CFT).

- Singapore-incorporated banks are subject to a mandatory five-year rotation of external auditors[Corporate Governance -Practice and Issues. MAS Notices to Banks (e.g., No 615) issued under the Banking Act specify that banks cannot appoint the same audit firm for more than five consecutive financial years without prior written MAS approval.

- MAS can initiate winding-up applications for banking companies whose license has been revoked or that have operated in violation of banking law. The Monetary Authority of Singapore may apply for the winding-up of a banking company if its license has been revoked or it has operated in contravention of banking law.

- Banking corporations, along with other MAS-regulated entities, use MASNET for electronic submissions of financial regulatory forms, notifications, and to access MAS communications.

- MAS issues detailed notices and directives to banks and other financial institutions. These cover extensive requirements for:

- Interactions with Other Legislation

- Companies Act (Cap 50): A “banking corporation” is referenced in various provisions, such as those related to shareholdings and powers to require information about interested persons in shares or debentures. The Minister responsible for administering the Companies Act is not authorised by Section 8A to call for the production of books of a banking corporation or conduct investigations into them under Section 8F. This is because the control over such entities falls under the Monetary Authority of Singapore. Loans made by companies regulated by banking laws, finance companies, or insurance, or supervised by MAS, are not prohibited when made in the ordinary course of business.

- Income Tax Act 1947: This Act refers to banks licensed under the Banking Act as “prescribed financial institutions” for certain tax provisions. It also exempts financial institutions, including banks, from certain tax implications on specific income derived from approved syndicated offshore credit or guarantee facilities. Loans made by a bank or finance company are also relevant for tax deductions on provisions for doubtful debts.

- Payment Services Act 2019 (PS Act): The PS Act regulates various payment services, and entities applying for a payment services license might also intend to conduct other activities regulated by MAS, such as financial advisory. MAS notices on AML/CFT, applicable to payment service providers, include requirements for correspondent accounts, which may involve banking relationships.

- Securities and Futures Act (SFA): Banks licensed under the Banking Act are “specified financial institutions” and certain offers of securities by them may be subject to specific regulations or exemptions under the SFA. Deposits with licensed banks are generally not considered “debentures” for the purposes of Part XIII of the SFA, as their regulation falls under the Banking Act. Fund managers holding a banking license under the Banking Act were previously required to issue a statement that carried the same liabilities as a prospectus for public issues of interests.

In summary, banking licenses in Singapore are a vital component of the financial regulatory framework, issued and stringently overseen by the MAS through the Banking Act and a web of interconnected legislation and directives, ensuring the sector’s stability and proper conduct.