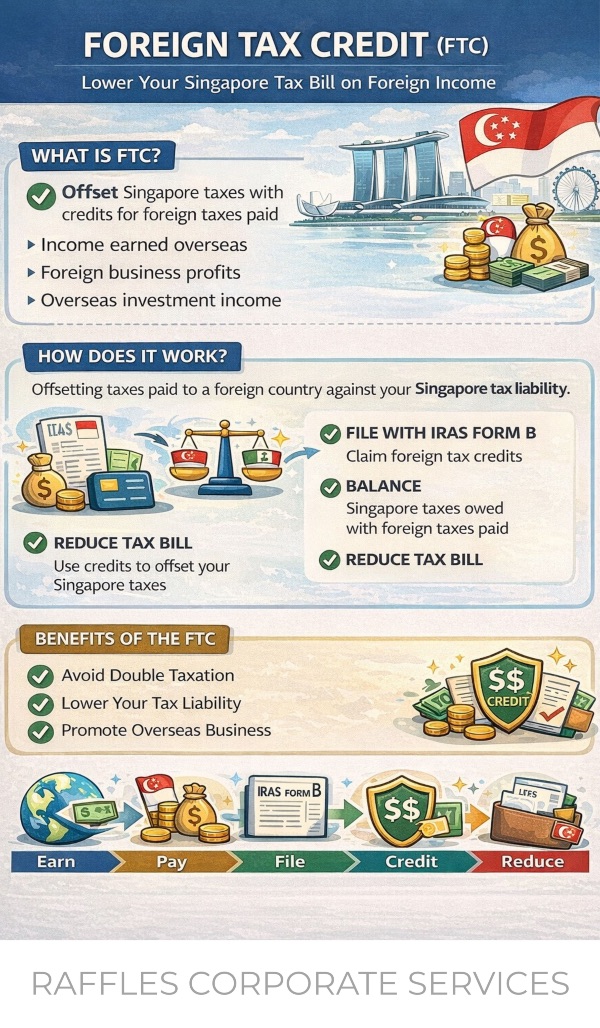

Definition

Foreign Tax Credit (FTC) Singapore refers to a tax relief that allows Singapore tax residents to offset foreign taxes paid against Singapore tax payable on the same income. Therefore, it prevents double taxation when income is earned overseas and taxed both abroad and in Singapore.

When it matters

- When a Singapore company earns foreign-sourced income (e.g., dividends, interest, service income).

- When overseas withholding tax has already been deducted before funds reach Singapore.

- When claiming relief under a Double Taxation Agreement (DTA) or unilateral tax credit.

- When filing Estimated Chargeable Income (ECI) or Form C/C-S for the Year of Assessment (YA).

- When remitting foreign income into Singapore (subject to current tax exemption rules).

Key requirements & process (Singapore)

Eligibility criteria

- The company must be a Singapore tax resident.

- Additionally, the same income must be taxed in both a foreign jurisdiction and Singapore.

- Therefore, the foreign tax must be legally payable (not voluntary).

- Meanwhile, the income must be taxable in Singapore (i.e., not exempt).

Types of FTC in Singapore

- DTA FTC: Applies where Singapore has a tax treaty with the foreign country.

- Unilateral FTC (UTC): Applies even if no DTA exists.

- FTC pooling: Allows combining foreign taxes across multiple sources to simplify claims.

How to claim FTC

- Determine taxable income

Identify foreign income subject to Singapore tax. - Compute foreign tax paid

Use actual withholding tax or assessed foreign tax. - Apply FTC limitation

The credit is capped at the Singapore tax payable on that foreign income. - File via IRAS

Submit claims through Form C/C-S on myTax Portal. - Prepare supporting documents

- Foreign tax certificates

- Withholding tax statements

- Proof of income received

Worked example (SG context)

A Singapore company earns S$100,000 in consulting income from Indonesia. Indonesia withholds 10% tax (S$10,000). Therefore, the company reports the full S$100,000 in Singapore.

Assuming Singapore tax on that income is S$17,000, the company can claim FTC of up to S$10,000. As a result, the net Singapore tax payable becomes S$7,000.

Common pitfalls & tips

- Claiming on exempt income: FTC is not allowed if income qualifies for foreign-sourced income exemption.

- Missing documentation: IRAS may reject claims without proper tax certificates.

- Incorrect pooling: FTC pooling rules must be applied correctly across similar income types.

- Overclaiming credits: FTC cannot exceed Singapore tax payable on that income.

- Timing mismatch: Ensure foreign tax and income are recognised in the same YA.

Practical tips:

- Keep withholding tax vouchers and foreign tax assessments.

- Additionally, verify DTA rates before calculating FTC.

- Meanwhile, review IRAS updates annually as rules may change.

FAQs

Q1. What is the difference between DTA FTC and unilateral FTC?

A1. DTA FTC applies when Singapore has a tax treaty with the foreign country. However, unilateral FTC applies when no treaty exists, subject to IRAS conditions.

Q2. Can FTC exceed Singapore tax payable?

A2. No. Therefore, the maximum FTC is capped at the Singapore tax payable on the same income.

Q3. Do I still need FTC if income is exempt?

A3. No. If foreign-sourced income qualifies for exemption under IRAS rules, FTC is not applicable.

Q4. What is FTC pooling?

A4. FTC pooling allows companies to combine foreign taxes from multiple sources, simplifying claims and potentially maximising credits.

Q5. Where do I claim FTC?

A5. You claim FTC when filing corporate tax returns (Form C or C-S) via IRAS myTax Portal.